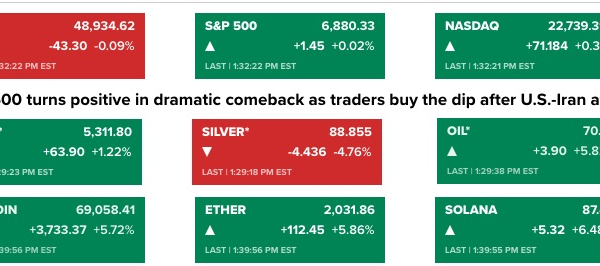

The cryptocurrency markets faced significant fluctuations this week, transitioning from a relief rally spurred by the end of a prolonged US government shutdown to a broader risk-off sentiment. This shift was largely influenced by declining performance in artificial intelligence (AI) stocks, disappointing macroeconomic data, and hawkish remarks from Federal Reserve officials. Notably, Bitcoin dipped below $98,000, marking its lowest level since May.

During this turbulent period, gold reached a new one-month high, enjoying a seven-day winning streak before experiencing a selloff on Thursday. The simultaneous decline of US equities, Treasuries, and commodities alongside cryptocurrencies highlighted systemic market stress. However, a liquidity influx exceeding $100 billion from the Treasury General Account (TGA) is anticipated, which has historically provided a supportive backdrop for Bitcoin.

Market Performance Overview

Throughout the week, the crypto market exhibited erratic behavior. On Monday, optimism reigned as traders anticipated the end of the 43-day government shutdown. Yet, by Thursday, Bitcoin sharply reversed its gains, driven down by a broader risk-off trend linked to AI stock performance. In contrast, altcoins displayed varied reactions; XRP surged by 8.5% following multiple exchange-traded fund (ETF) approvals, while privacy tokens like Zcash (ZEC) saw significant corrections, plummeting from $764 to around $500.

Potential CFTC Approval and Market Implications

Acting CFTC Chair Caroline Pham has indicated ongoing discussions with US exchanges regarding the launch of leveraged spot trading for Bitcoin and Ethereum as early as next month. This development marks a significant regulatory shift, allowing retail investors to engage in these products under strict risk and margin controls. The potential integration with the SEC aims to clarify regulatory boundaries, with stablecoins possibly being approved as tokenized collateral in 2026. Should these products launch, they could unlock approximately $50 billion in new capital, equating to the total inflows from spot Bitcoin ETF investments observed from January to July 2025.

Global Market Dynamics

In the equities market, a notable rotation occurred away from AI technology stocks as doubts about the sustainability of the AI growth narrative emerged. Key factors contributing to the AI sector”s downturn included infrastructural challenges, rising credit stress reflected in Oracle”s debt downgrade, and intensified competition from major Chinese firms like Alibaba and Tencent. As a result, investors shifted their focus toward healthcare and financial sectors, with healthcare stocks achieving nine consecutive sessions of gains.

On the currency front, the US dollar exhibited weakness, particularly against the Japanese yen, which broke above 155 despite lower yields. Commodities also faced pressure, with oil prices declining by 3% amid OPEC”s supply revisions and ongoing geopolitical negotiations. In the bond market, the 10-year Treasury yield rose from 4.06% to 4.11%, while volatility, which had fallen post-shutdown, spiked again to approximately 20 as AI stocks faced further selling.

Macro Economic Outlook

The decline in risk appetite can be attributed to several factors. First, cracks in the AI megatrend have emerged, as narratives of boundless growth give way to concerns over power limitations, leveraged balance sheets, and increased competition. Additionally, macroeconomic data has shown signs of deterioration, with private job losses reported at around 45,000 in October and Goldman Sachs predicting a 50,000 drop in non-farm payrolls, marking the worst performance since December 2020. Finally, hawkish commentary from various Federal Reserve officials has cast doubt on previously high expectations for interest rate cuts.

Looking ahead, the anticipated liquidity injection from the TGA could provide a significant boost to risk assets, including Bitcoin. Historically, when TGA balances decrease by more than $80 billion, Bitcoin has risen 61% of the time, with an average gain of 8.8%. This trend suggests a favorable outlook for the leading cryptocurrency in the coming weeks.

Upcoming events to watch include Nvidia”s earnings report on November 19, which could trigger a tech-led correction if results fall short of expectations. Additionally, a backlog of US macroeconomic data from September and October is set to be released, potentially impacting market sentiment further. The looming risk of another government shutdown in January due to expiring temporary funding adds another layer of uncertainty to the market.

In summary, while short-term liquidity dynamics and gold”s historical lead suggest a stabilization of Bitcoin into late November, the medium-term outlook remains clouded by concerns over AI sector fragility, weak macroeconomic data, and a hawkish Federal Reserve stance. In the long run, the potential approval of leveraged trading for Bitcoin and Ethereum by the CFTC could introduce a significant liquidity shock to the market.