In a provocative analysis, Joe Burnett, the Vice President of Bitcoin Strategy at Strive (Nasdaq: ASST), has put forth a bold prediction that Bitcoin could skyrocket to $11 million by the first quarter of 2036. This forecast is not predicated on the idea of Bitcoin replacing existing financial systems, but rather on its potential to emerge as the leading long-duration savings asset in an economy transformed by artificial intelligence (AI)-induced deflation and ongoing monetary expansion.

Burnett elaborated on his thesis in a note published on March 2, suggesting that the cryptocurrency should be viewed not merely as a speculative investment but as a prime candidate for absorbing excess liquidity in an environment defined by falling production costs and persistent policy interventions. His base scenario estimates the Bitcoin network could attain a valuation of approximately $230 trillion by 2036. This projection is juxtaposed against a global financial asset base that he anticipates will increase from over $1 quadrillion today to around $1.97 quadrillion in the next decade, assuming a 7% annual growth rate.

Within this framework, Burnett posits that Bitcoin could represent roughly 12% of total global financial assets. He states, “That outcome reflects a measured repricing of global wealth toward the only monetary asset with absolute scarcity.” According to him, Bitcoin need not replace all currencies or be used universally for daily transactions; it simply has to establish itself as the primary long-term savings vehicle in a world characterized by continuous monetary expansion and technological deflation.

The AI Deflation Engine

At the heart of Burnett”s argument is what he refers to as the “AI deflation engine.” He asserts that advancements in AI will lead to reduced labor costs, accelerated output, and heightened competition across both digital and traditional sectors, exerting sustained downward pressure on prices. He draws a parallel to the historical transition from horses to automobiles, emphasizing that this time the focus is on white-collar jobs.

Burnett notes that AI technologies are already capable of performing tasks such as drafting contracts, analyzing financial data, and writing code—functions that were previously the domain of junior professionals. Meanwhile, robotics are making significant inroads into logistics, manufacturing, and agriculture. In a neutral monetary environment, such a productivity surge would typically enhance real purchasing power. However, within a debt-based fiat system, it introduces instability.

The combination of declining wages, weakening asset prices, and fixed nominal liabilities creates a precarious scenario. Burnett argues that as AI drives real-economy deflation, central banks will likely respond by increasing liquidity to stave off a deflationary spiral. This response could set off a cycle where initial moves toward cash and government bonds transition into rate cuts, balance-sheet expansion, and fiscal transfers.

Bitcoin”s Unique Position

Burnett points to historical events in 1987, 2001, 2008, 2020, and 2022 as evidence that policymakers are averse to prolonged deflation. He believes that the long-term outcome will be a combination of persistent productivity deflation and ongoing monetary expansion, which will leave capital searching for an asset whose supply cannot be manipulated by political forces. This, he argues, is where Bitcoin stands apart.

Equities, according to Burnett, face increasing risks from AI-driven market disruptions. While real estate maintains its scarcity value, advancements in technology may streamline design and construction processes, potentially suppressing long-term price appreciation. Sovereign bonds may provide nominal stability but remain tied to currencies that are subject to ongoing devaluation.

In contrast, Bitcoin”s capped supply, divisibility, portability, and verifiability position it as uniquely qualified to absorb global liquidity over time. Burnett also introduces a concept he calls “Digital Credit,” which refers to income-generating financial instruments backed by substantial Bitcoin holdings. He cites publicly traded entities like STRC and SATA as examples that offer dollar income to credit investors while simultaneously facilitating Bitcoin accumulation.

Burnett emphasizes the scarcity dynamics at play, noting that by 2036, fewer than 41,000 new BTC will be generated throughout the year. If global financial assets are projected to reach around $2 quadrillion and merely 1% of one year”s incremental capital formation seeks monetary preservation in Bitcoin, this could yield $1.4 trillion competing for the limited new supply—translating to about $34 million of demand for each newly minted coin.

Though he acknowledges that the path to this outcome may not be linear, Burnett insists that Bitcoin”s journey toward eight-figure prices will ultimately reflect structural monetary conditions rather than speculative fervor or “faith.” As liquidity continues to expand in a technologically deflationary landscape, he argues that capital will increasingly gravitate toward assets that can maintain value over time.

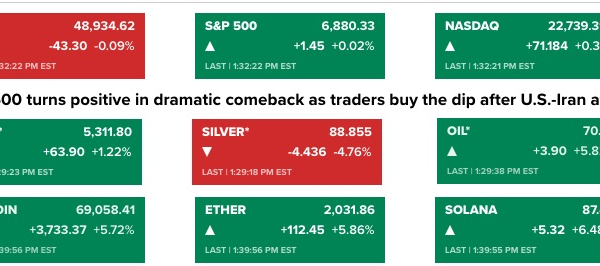

As of the latest data, Bitcoin was trading at $66,958, highlighting the current market dynamics as it navigates through this transformative phase.